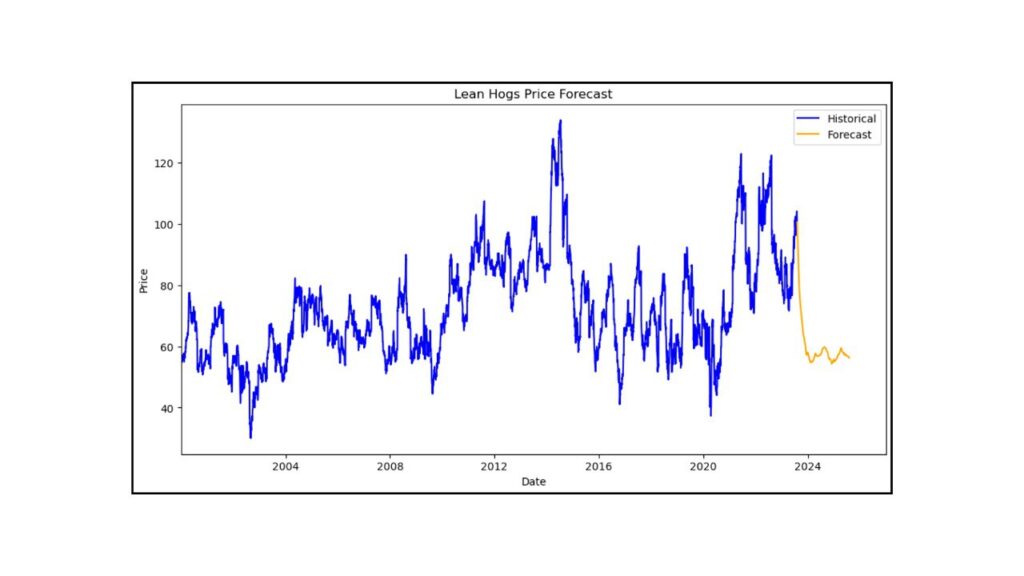

Commodity Forecasting Project

This school project for the module Manufacturing Services & Operations involved developing a comprehensive, multi-algorithm forecasting system designed to mitigate financial risks stemming from volatile commodity price fluctuations caused by geopolitical and economic instability. The model integrates with Enterprise Resource Planning (ERP) systems made by other classmates to provide stakeholders—including government bodies and private firms—with high-accuracy price predictions for strategic policy-making and competitive market positioning.

Core Impact & Responsibilities

Multi-Model Forecasting Model: Evaluated and implemented four distinct forecasting methods—AutoGluon, SARIMA, Prophet, and Transformers—to handle diverse data types ranging from simple seasonal patterns to complex, long-range dependencies.

Dynamic Model Selection: Engineered an evaluation subsystem that automatically selects the highest-performing model for a given dataset by comparing metrics such as Akaike Information Criterion (AIC) and Mean Squared Error (MSE).

Advanced Ensemble Learning: Leveraged AutoGluon to develop a Weighted Ensemble model, which reduced overfitting and lowered error rates by combining predictions from multiple underlying architectures, including linear regression and neural networks.